In other words, what is the Quick Ratio?

As a measure of a company’s capacity to satisfy its short-term commitments using its most liquid assets, the quick ratio is a useful indication of its liquidity situation.

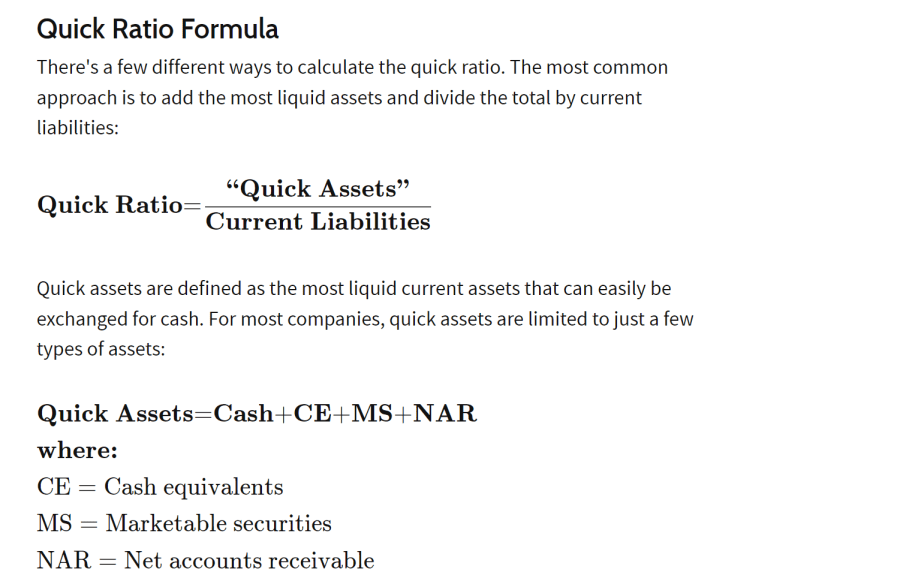

Quick Ratio Formula

Contents

This ratio is also known as the acid test ratio because it demonstrates a company’s liquidity by comparing its short-term debt to its short-term assets. In informal contexts, a “quick test” or “acid test” is a test that is intended to provide immediate findings.

NOTABLE CONCLUSIONS

A company’s ability to meet its short-term obligations (its “immediate liabilities”) without liquidating its inventory or taking on more debt is measured by the quick ratio.

The current ratio, which uses all current assets to pay all current liabilities, is seen as a less conservative metric than the quick ratio.

The quick ratio is determined by dividing the sum of a company’s current liabilities by its most liquid assets, which include cash and cash equivalents, marketable securities, and accounts receivable.

Specifically omitted are current assets that are neither readily converted to cash or would need steep discounts to be liquidated, such as prepaids and inventories.

If the ratio is high, the firm is solvent and financially sound; if it is low, it is likely to have trouble making its debt payments.

The Quick Ratio – Everything You Need to Know

The quick ratio evaluates a company’s liquidity by comparing its current assets to its short-term obligations.

In contrast to the company’s current liabilities, which are debts or obligations required to be paid to creditors within one year, the company’s liquid assets are those current assets that may be easily converted into cash with little influence on the price obtained on the open market.

- The usual quick ratio yields a value of 1. It means the corporation has precisely the amount of liquid assets needed to settle its present debts.

- If a company’s quick ratio is less than 1, it may not have enough short-term cash on hand to cover all of its current debts, but if it’s more than 1, it can eliminate those debts immediately.

- For instance, if a corporation has a quick ratio of 1.5, it means that for every $1 in current obligations, it has $1.50 in liquid assets.

Insight into the viability and some characteristics of a company may be gained from such numerical ratios, but they may not provide a full picture of the firm’s health. To get an accurate view of a business’s financial health, it’s crucial to include a wide range of related metrics.

Elements That Make Up the Fast Ratio

The cash available component of the fast ratio is one of the simpler parts. It is important for a business to verify that their cash on hand agrees with the bank statements they get on a regular basis.

A portion of this component may be in the form of cash, which may be in the form of currency of several nations after being converted to a common currency.

Money or Its Par Value

The assets held in a cash equivalents account are often relatively low risk and very liquid, making them a convenient and useful complement to traditional cash.

Cash equivalents may include, but are not limited to, the following: Treasury bills, certificates of deposit (with consideration for early withdrawal penalties), bankers’ acceptances, corporate commercial paper, and other money market products.

Digital assets, like as bitcoin or digital tokens, may not be described as cash or cash equivalents in AICPA publications.

Investable Assets

Generally speaking, marketable securities do not have any such time-sensitive dependencies. The amount expected to be paid in 90 days or fewer under normal circumstances should be used for the computation, nevertheless, so as to preserve accuracy.

Early withdrawal or liquidation of assets, such as interest-bearing securities, may result in fines or a reduction in book value.

Cash Receipts Net

- Accounts receivable’s potential as a source of available cash relies on the company’s policies on customer credit.

- Compared to a corporation that allows its clients 90 days to make payments, one that requires upfront payments or permits just 30 days would have more cash on hand.

- Liabilities might be recorded for a longer period of time if, instead of receiving payments from consumers immediately, the corporation negotiated shorter payment terms with its suppliers.

- It may improve its quick ratio and its ability to meet its current obligations if it could turn accounts receivable into cash more quickly.

Reduce the overall accounts receivable balance by the projected amount of bad debt. As the goal of the quick ratio is to indicate potential cash on hand, unanticipated receivables should be left out of the calculation.

Related Search Post:

Accounts Payable Right Now

Unlike the current ratio, which attempts to differentiate between when payments may be due, the fast ratio includes all obligations that have an immediate payment date.

All current obligations with a near-term due date are assumed for the quick ratio calculation. Accounts payable, salaries due, current sections of long-term debt, and tax payable are all components of a company’s current obligations.